Why Australia’s Gas Market Is Entering a More Operational Era

Out in Australia, the conversation around gas feels different than it did even a few years ago. It’s less about discovery and more about durability. Less about how much resource sits underground and more about whether the system can actually keep up when demand starts leaning harder against supply.

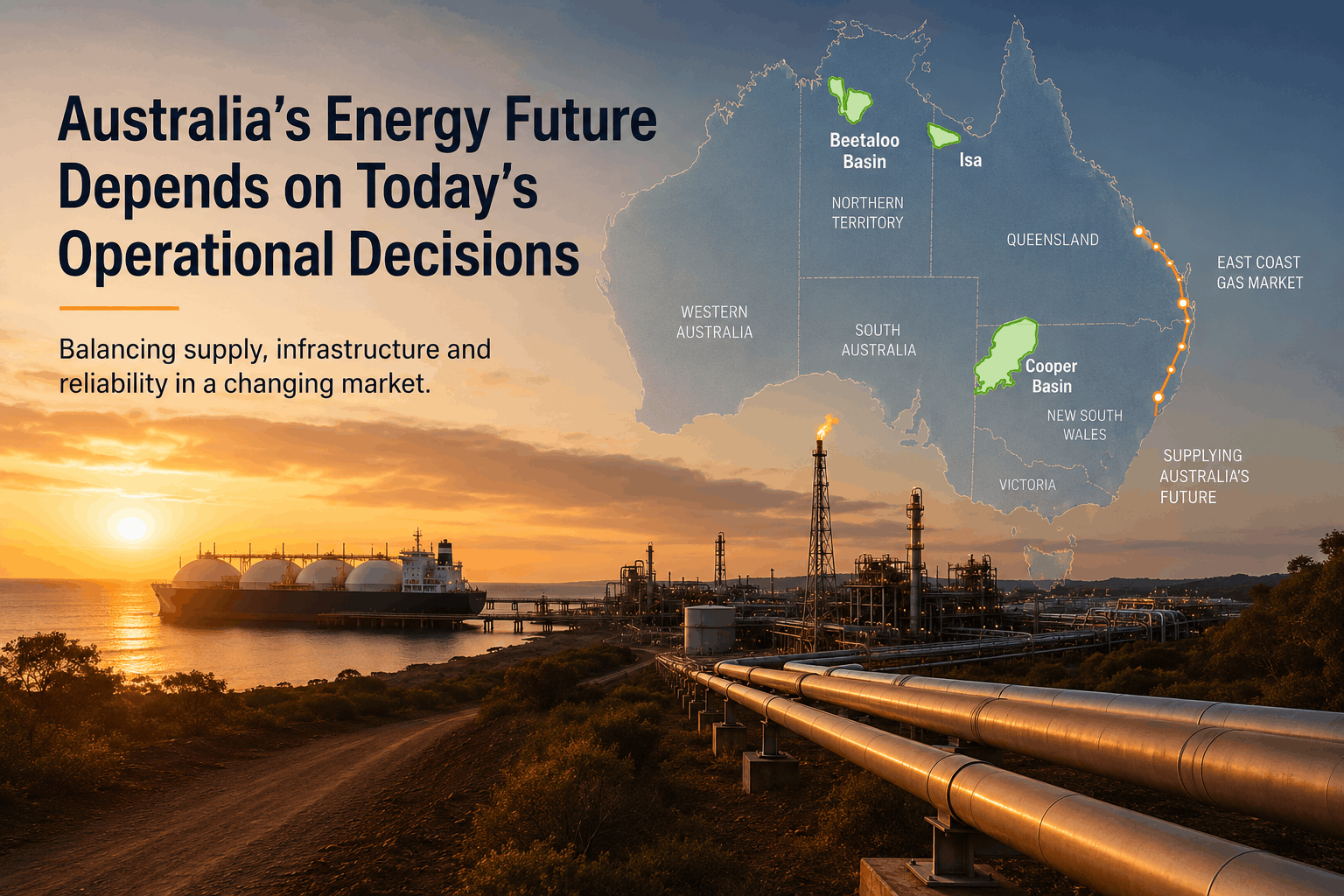

You can see it in the East Coast market already. Legacy production from Bass Strait continues to decline, while manufacturers, utilities, and regulators are all trying to figure out what reliable supply looks like over the next decade. The concern isn’t really about one bad season. It’s about whether the infrastructure, storage, and upstream investment pipeline can move fast enough to avoid tighter winter markets becoming the norm instead of the exception.

Why Northern Territory Projects Are Drawing Attention

That’s part of why the Northern Territory keeps coming up in energy discussions now. The Beetaloo Basin has shifted from being viewed as a long-range shale prospect to something policymakers and operators are watching much more closely. Not because anyone believes it solves every problem overnight, but because new domestic supply matters more when older fields start carrying less of the load.

For people working in the industry, the shift feels familiar. It’s not a boom atmosphere. It’s more measured than that. Operators are moving carefully, balancing drilling programs against financing conditions, infrastructure constraints, regulatory reviews, and long-term commodity pricing. The work still moves forward, but with more discipline around timing and execution.

Several operators active in the Beetaloo Basin, including Tamboran Resources, are advancing projects tied to future east coast supply discussions. But even there, the reality is more complicated than headlines sometimes suggest. Pipeline buildout, environmental approvals, labor availability, methane requirements, and commercial economics all still matter. None of it is automatic.

The Debate Is Becoming More Operational

That’s really the bigger story taking shape across Australia right now. The debate is becoming less ideological and more operational. How do you maintain grid reliability while renewables continue scaling? How do you balance export obligations with domestic supply pressure? And how do you build enough infrastructure capacity before the market tightens further?

There probably isn’t one single answer. More likely, it ends up being a mix of storage, transmission, dispatchable generation, LNG coordination, and selective upstream development working together over time.

Flexibility Is Becoming Part of the Strategy

What’s changing is that flexibility itself is becoming part of the energy strategy. Not just for operators and regulators, but for manufacturers, infrastructure planners, and regional economies trying to navigate a market that no longer feels as predictable as it once did.

This article is for informational purposes only and does not constitute financial, investment, or regulatory advice. Forecasts and project timelines are subject to change based on market and regulatory conditions.